From the Moon and Back: Has the Iran War changed our outlook for the markets?

Equities – both domestic and international – sold off. From peak to trough the S&P 500 pulled back 8.6%, the Nasdaq pulled back 9.4%, and international stocks pulled back 11.4%. The price of oil spiked over 100% at its worst. Yields rose on the expectation of higher inflation, pushing bond prices down. Yet, with the announcement of a ceasefire, prices rallied back with vengeance. It’s as if the markets have been to the moon and back. So, the question begs, what now? Have expectations around market returns and risks changed?

Key Takeaways

• Even though the war in Iran led to an increase in volatility in equities, we are still generally positive on equities – especially international stocks.

• Multiple Federal Reserve rate cuts and the corresponding drop in yields isn’t as likely as it was pre-war.

• Commodities – especially oil and natural gas – are the assets seeing the largest price increases from the war.

We went into the year with a relatively strong, albeit slowing, economy and were cautiously optimistic on financial markets. In 2025, bonds had their best year since 2020 – up over 7%. We expected another rate cut in 2026 to stimulate a slowing economy and further support bond prices. Gold also hit it out of the park in 2025, returning over 60%; yet, we still expected a slight drop in yields and continued global central bank buying of gold to act as support for prices in 2026. Finally, but not least, amid the frothy valuations and roughly 16% return in large cap domestic stocks in 2025, we saw opportunities going forward in international stocks, small cap stocks, and value stocks with their more attractive valuations.

We also attempted to avoid the cracks in the markets for our clients – there were signs of stress in private credit, which was at risk of spreading to the public high yield corporate bond market. Likewise, large cap growth stocks and the AI theme appeared to be losing steam as investor concerns about overinvestment and high price multiples were boiling to the surface. Again though, we were cautiously optimistic that there would be opportunities for good returns while prudently avoiding the riskier areas of the markets with poor valuations.

Then came the war in Iran and everything flipped. Equities – both domestic and international – sold off. From peak to trough the S&P 500 pulled back 8.6%, the Nasdaq pulled back 9.4%, and international stocks pulled back 11.4%. The price of oil spiked over 100% at its worst. Yields rose on the expectation of higher inflation, pushing bond prices down. Yet, with the announcement of a ceasefire, prices rallied back with vengeance. It’s as if the markets have been to the moon and back. So, the question begs, what now? Have expectations around market returns and risks changed? Below we will walk through what has changed, including rising risks, and what has stayed same in each asset class.

The Stock Market

Although our base case for 2026 has slightly shifted due to the war, we remain generally still positive on equities. We prefer international stocks to domestic stocks, have developed a slight preference for value stocks to growth stocks, and find some parts of the small cap stock market attractive. That said, there is a risk of the Iran War dragging on longer and further attacks on energy infrastructure than what markets have priced in. In that tail risk scenario, stocks would likely pull back again, leading us to lower our return expectations for equities this year.

Let’s take a pulse on where stocks are now. Given the recent rally from the Iran War ceasefire, international stocks are up 9.3%, US small cap stocks are up 9.5%, and US large cap stocks are up 2.3%.

Performance YTD: US Large Cap, US Small Cap, International ex. US

Source: YCharts. State Street SPDR S&P 500 ETF Trust, State Street SPDR Portfolio S&P 600 Small Cap ETF, iShares MSCI ACWI ex US ETF, Performance YTD. Daily Return Data YTD as of 4/14/2026. Past returns don’t guarantee future results.Within large cap stocks more specifically, there’s significant churn underneath the surface. Capital is shifting out of sectors with lofty valuations like software companies and the communication services sector more broadly in favor of consumer staples, industrials, and energy.

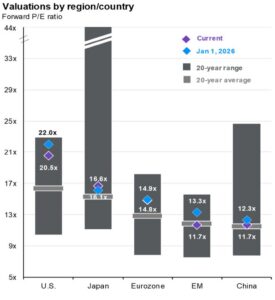

Even though international stocks pulled back the most peak to trough when the Iran War first kicked off, they still have attractive valuations. Many international stock indices are trading at price to earnings ratios much closer to their 20-year average and significantly below U.S. valuations. If the dollar were to weaken again this year, it would further boost international returns for US investors. As such, we are generally considering any pullbacks in international stocks due to the war as buying opportunities.

International Valuations are More Attractive than Domestic

The Bond Market

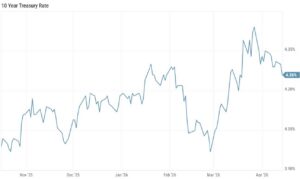

Zeroing in on bonds, we are not as optimistic as we once were for a drop in yields to support prices in the space. Markets went from pricing in 1-2 rate cuts for 2026 to pricing less than 1 rate cut in for this year with only a 30% chance of a cut before year end as of 4/14/2026. What caused the change? The rise in yields on the expectation of higher inflation from the spike in oil prices.

10 Year Treasury Yields Spiked at the Start of the War

One can see this playing out in the latest Consumer Price Index (CPI) release. CPI is the most commonly used measure for inflation in the US and it rung in at 3.3% year over year in March – up from 2.4% the month prior. According to research by the Federal Reserve, an increase in oil prices due to a supply shock translates to a 30 bps rise in core CPI on average over the course of eight quarters. We are anticipating a further inch up in inflation, including in core CPI.

US Consumer Price Index

The increased volatility around expectations for inflation, yields, and Federal Reserve policy will set a backdrop for the potential for higher volatility in bonds throughout the remainder of the year as markets tease out the impact from the war in Iran. That is why we prefer to invest in shorter-term bonds with lower sensitivity to the movement in yields for the time being.

We also find municipal bonds and mortgage-backed securities (MBS) attractive areas of the market. Municipalities still have pretty good balance sheets, and the MBS market is benefiting from a slightly lower sensitivity to any movement in yields. In the tail risk scenario where yields rise much higher than expected, we would likely lower exposure to MBS though.

Generally, we are staying away from private credit and are cautious on public high yield credit. Coming off extremely rich valuations, credit spreads relative to Treasuries widened at the start of the Iran War, and we consider them vulnerable to further widening given ongoing concerns about tech exposure and lack of liquidity. Some major private credit funds and business development companies (BDCs), or vehicles used to get access to diversified private credit, have been forced to sell some of their assets for liquidity needs, putting downward pressure on prices. The S&P BDC Index is down 11.8% year to date as of 4/13/2026.

Alternatives

One could argue that commodities are where all the action has been this year. Year to date, the all-stars have been oil, up 80.5%, European natural gas, up 64.28%, and gold, up 10.3%. This is quite the change from what we expected going into the year – we did not expect oil or natural gas to be up more than 15-20%. It goes without saying, but the rise in oil and natural gas prices are supported by a significant supply shortage. In natural gas in particular, prices are expected to remain elevated for years. Qatar Energy, the largest LNG exporter, mentioned that it may take 3 to 5 years to rebuild damaged natural gas infrastructure from the war.

European Natural Gas Futures Prices Have Increased Since the War

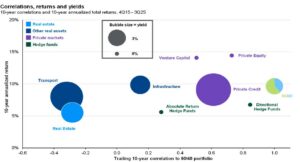

As for other alternatives, we tend to find infrastructure as one of the more

attractive areas to invest in within the private markets. Infrastructure provides predictable cash flows and incremental capital appreciation as their balance sheets improve through the life of the project. Historically, infrastructure tends to have higher returns than private real estate, and a low correlation to a stock/bond portfolio, meaning there may be diversification benefits.

Asset Class: 10 Yr Returns, Correlations, and Yield

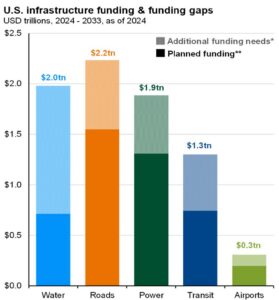

As many already know, there are large funding gaps in many areas of infrastructure in the U.S. – water, roads, power, and transit have some of the largest funding needs. This naturally opens up opportunities for investors when it’s the right business model.

Projected Infrastructure Funding (2024-2033)

We find regulated essential services attractive, such as contracted energy production and distribution, water utilities, and transit. Our view on these assets is driven by strong fundamental tailwinds, in particular, the large-scale infrastructure build-out to power artificial intelligence, as well as the monopoly-like business models that regulated utilities provide. We also like the built-in inflation mechanisms, like cost-pass through and in the case of utilities, rate-cases.

Summary

Although much has changed since the war in Iran, including the shift in expectations for Federal Reserve rate cuts and the spike in oil and natural gas, asset prices are moving back to trend. Equities have rebounded sharply and we are generally optimistic – especially with international stocks. We are a little less optimistic about fixed income, but that doesn’t mean there aren’t still opportunities and that bonds will have a bad year. We still like shorter-term bonds, MBS, and munis. Infrastructure is an area of private markets we still find attractive while being bearish on private credit. Risks to our current outlook include another sell off in stocks if the war in Iran worsens, a further rise in yields if inflation creeps too high, and contagion risks from private credit to other areas of the private markets or public high yield credit.

Disclaimer

Advus Financial Partners, LLC is an investment advisory firm registered with the Securities and Exchange Commission (“SEC”) under the Investment Advisers Act of 1940. Registration as an investment adviser does not imply a certain level of skill or training. The oral and written communications of an adviser provide you with information about which you determine to hire or retain an adviser. For more information please visit: https://adviserinfo.sec.gov and search for our firm name. This market update and commentary has been provided for informational purposes only and is not intended as legal, tax, or investment advice, or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of publication and are subject to change without notice. Past performance is not indicative of future results.

To download a copy of this article, click here.